আরও দেখুন

24.12.2024 01:53 PM

24.12.2024 01:53 PM

The major U.S. stock market indexes continued to rally on Monday. The Dow Jones Industrial Average and Nasdaq Composite ended the day with positive results, extending their winning streak to three trading sessions. The key factor pushing the market higher was the strengthening of the leading tech giants, known as the "Magnificent Seven."

Mega-cap companies had a significant impact on the market, especially in the low investor activity typical of the holidays. Their gains were even more noticeable against the backdrop of a decline in overall trading volume. On Monday, U.S. exchanges recorded a movement of 12.76 billion shares, which is significantly lower than the average of 14.89 billion shares over the past 20 trading days.

The companies that contributed to the rise included giants Meta Platforms (banned in Russia), Nvidia and Tesla, whose shares rose by 2.3-3.7%. Other leaders were not far behind: Apple, Amazon.com and Google's parent company Alphabet. Their results also contributed to the positive dynamics.

The growth of tech stocks helped the Nasdaq Composite and Dow Jones Industrial Average to consolidate their winning streak, and the S&P 500 ended the day with an increase for the second time in the last three sessions.

These data highlight the importance of the influence of the largest tech companies on the market, especially during periods when investor activity is declining. Confidence in the future of the tech sector has once again become an important driver for Wall Street.

The main US stock indices ended another session with significant growth. The S&P 500 added 43.22 points (+0.73%) to 5974.07, the Nasdaq Composite increased 192.29 points (+0.98%) to 19764.89, and the Dow Jones Industrial Average rose 66.69 points (+0.16%) to end the day at 42906.95.

The November rally, triggered by the presidential election results, continued to gain momentum, but December was the month when markets reached their peak. Additional impetus was provided by the Federal Reserve's revised forecasts. Now, instead of four expected rate cuts of 25 basis points in 2025, the regulator forecasts only two. At the same time, the forecast for annual inflation was raised, which forced investors to revise their expectations.

While there is optimism, there is also caution in the market. On Wednesday, the Federal Reserve signaled a slower rate cut, which triggered a wave of sell-offs. However, this short-term cut did not break the general mood: investors continue to focus on the long-term prospects related to economic stability and monetary policy regulation.

The rise in indices indicates market participants' confidence in the US economy, despite the uncertainty regarding inflation and rates. Both monetary policy and the actions of large companies that form the basis of the stock market remain in the spotlight.

Many analysts are encouraged by the stability with which markets react to external challenges, which gives grounds for confidence in further strengthening of the positions of key indices.

The positive dynamics in the stock market continue despite recent adjustments in interest rate expectations. As Chris Zaccarelli, chief investment officer at Northlight Asset Management, noted, the rate outlook has changed, but the underlying trends remain unchanged. Tech and innovation stocks continue to find support, underpinning the overall gains.

Monday ended with solid gains for most S&P 500 sectors, with eight out of 11 sectors showing positive dynamics. The day's leader was communications services, which rose 1.4%. This sector is proving its importance, reflecting the continued interest in modern technology and digital services.

The market is entering the so-called Santa Claus Rally, a historically strong period for U.S. stocks. Since 1969, the last five days of the outgoing year combined with the first two days of the new year have averaged a 1.3% gain for the S&P 500, according to the Stock Trader's Almanac. That's traditionally a good time for investors, and current conditions are setting the stage for a repeat of that success story.

Chris Zaccarelli believes the market is now in a good position to hold on to rather than sell for tax breaks. This year's gains in stocks give investors confidence that they can reap more value in the long term.

The stock market is showing resilience and is poised to make gains despite corrections. Technology remains the growth engine, and the upcoming Santa Claus Rally provides additional reasons for optimism.

The stock market was a mixed bag on Monday, with tech giants and pharmaceutical companies taking center stage. Despite the mixed dynamics, the market is showing signs of resilience.

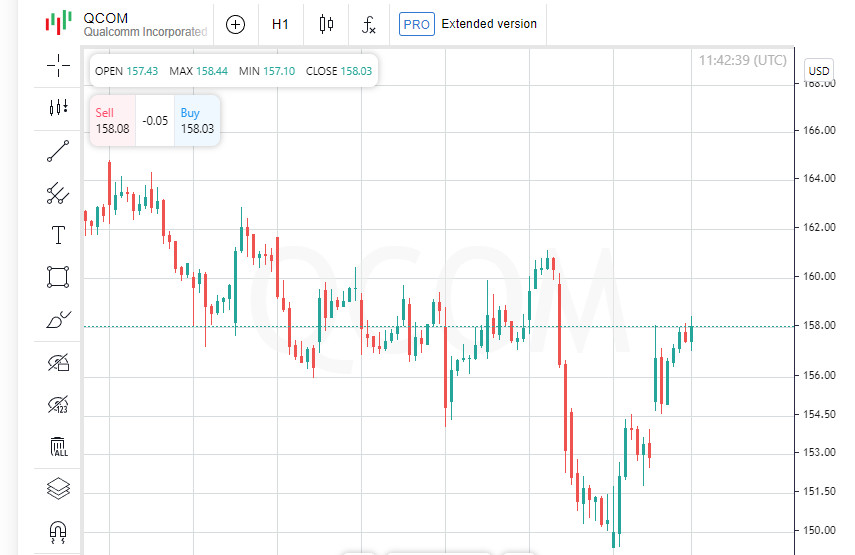

Qualcomm shares rose 3.5% after a court ruling in the company's favor. A jury ruled that Qualcomm's processors were properly licensed under an agreement with U.K.-based Arm Holdings. But the story is far from over: Arm intends to seek a review of the case. Its shares fell by 4% on the news.

The world's largest retailer Walmart came under pressure. Its shares fell by 2% after the US consumer finance regulator accused the company, along with Branch Messenger, of forcing more than a million couriers to use accounts that resulted in unwanted fees of more than $10 million. The scandal was a serious blow to the retailer's reputation and stock.

Pharmaceutical giant Eli Lilly showed a rise of 3.7% after the US Food and Drug Administration (FDA) approved a new drug for obstructive sleep apnea - Zepbound. This event pleased the company's investors, but hit the makers of medical devices for the treatment of apnea. ResMed and Inspire Medical shares fell 2.6% and 0.1%, respectively.

Department store chain Nordstrom also found itself in the spotlight, with shares down 1.5% on news that the company's founding family and Mexican retailer El Puerto de Liverpool had agreed to buy the company out and take it private.

Globally, stocks rose, helped by support from Wall Street. However, the bond market was a different story, with U.S. Treasury yields hitting a nearly seven-month high. Meanwhile, data showing deteriorating U.S. consumer confidence is causing investors to reassess expectations for a Federal Reserve rate cut in 2025.

The stock market continues to react to a mix of corporate news and macroeconomic cues, highlighting the complexity of the current investment environment.

The US Nasdaq and S&P 500 indices ended the day higher, largely driven by gains in tech stocks. In particular, Nvidia and Broadcom were the main drivers of the rally, once again confirming their status as industry leaders.

However, the overall picture on the market was overshadowed by the Conference Board report. The consumer sentiment index unexpectedly fell to 104.7 in December, which was significantly lower than economists' expectations (113.3) and the revised 112.8 in November. The main reason for the decline was concerns about the future business outlook.

In the US manufacturing sector, the data also showed a mixed picture. The volume of orders for key capital goods, including machinery, continued to rise in November, indicating that demand in this area remains strong. However, orders for durable goods fell by 1.1% after rising by 0.8% in October. Weakness in commercial aircraft orders played a key role in the decline, reflecting changes in the aviation industry.

Despite bearish signals in consumer sentiment and weakness in some manufacturing sectors, a rally in tech stocks helped support market confidence. Mega-cap stocks continue to play a key role in offsetting the negative impact of macroeconomic factors.

Investors are closely monitoring sentiment and economic data, but the overall direction of the market points to further gains, supported by support from the tech sector.

Monday brought mixed signals for investors, as large-cap stocks continued to rise, but weak consumer confidence and rising bond yields pose additional challenges for the stock market.

Robert Phipps, director of Per Stirling Capital Management, drew attention to the sharp rise in the yield on 10-year US Treasury bonds, which reached the highest level since the end of May. In his opinion, the key mark for investors is the 4.6% level. "If yields exceed this threshold, we could see further growth to 5%, which would be a serious test for the market," the expert said, noting that the reason for the growth was the policy of the Federal Reserve System (Fed), which is slowing down the reduction of rates.

Phipps emphasized that markets continue to adjust to a less accommodative monetary policy. Despite the successes in shares of large technology companies, the overall picture of US indices remains weak. Investors are assessing the possible consequences of the slowdown in the reduction of rates of the Fed, which is causing an increase in caution.

At a global level, the MSCI index, which tracks stocks around the world, rose 0.65% to 849.74. Europe's STOXX 600 also showed a small gain of 0.14%, highlighting the relative stability of European markets amid volatility in the US.

Ahead of a short trading week, investors continue to analyze the impact of last week's sharp sell-off in stocks. Tim Ghriskey, senior portfolio strategist at Ingalls & Snyder, noted that uncertainty remains a high risk. "Investors are concerned about the economic situation, the possibility of missteps by the Fed and questions about what steps Donald Trump will take after his inauguration," he said.

The market is in a difficult phase, with positive moves in individual sectors clashing with broader concerns about economic stability and future policy actions. Macroeconomic factors continue to shape investor sentiment, setting the stage for cautious trading in the coming days.

The U.S. Treasury bond market is showing a rise in yields, reaching record levels since late May. These changes are accompanied by active selling of short- and medium-term debt obligations by the U.S. Treasury Department, which is setting the tone for the market this week.

The yield on the U.S. 10-year bond rose by 6.7 basis points to 4.591%, up from 4.524% on Friday. Similar dynamics were shown by the 30-year bond, whose yield increased by 6.3 basis points to 4.779%. This growth underscores the tension in the debt market caused by active issuance of Treasury bonds.

A successful sale of $69 billion in two-year notes took place on Monday, part of a larger plan to issue $183 billion in coupons during the week. Strong demand for these bonds shows that investors are still hungry for short maturities.

Year yields on two-year notes, which typically respond to expectations about Federal Reserve policy, rose 3 basis points to 4.342%, up from 4.312% on Friday.

As bond yields rose, the dollar also strengthened. The dollar index, which measures the dollar against a basket of major currencies, rose 0.27% to 108.08.

The euro weakened 0.22% to $1.0406, while the Japanese yen also lost ground, with the dollar gaining 0.45% to 157.12.

Rising Treasury yields and a stronger dollar underscore the tension in financial markets. Investors are closely monitoring the Treasury Department and the Federal Reserve for signals on the long-term outlook for the economy. With bond markets in high gear, the dollar remains a safe haven for investors.

Commodity trading activity has slowed ahead of the holidays. Concerns about an oil supply glut next year and a stronger dollar have weighed on prices.

Oil prices ended the day slightly lower. U.S. crude (WTI) fell 22 cents (-0.32%) to $69.24 a barrel. Brent, the global benchmark, lost 31 cents (-0.43%) to $72.63 a barrel. The stronger dollar makes oil less attractive to foreign buyers, adding to pressure on prices, and worries about oversupply are growing amid signs of a slowing global economy.

The precious metals market also felt the impact of a strong dollar and rising US Treasury yields. Spot gold fell 0.39% to $2,610.66 per ounce, while US gold futures fell 0.67% to $2,611.10 per ounce.

High bond yields make gold investments less attractive, especially in the context of the holiday lull in the markets.

The decline in oil and gold prices highlights the general uncertainty in the commodity markets. Investors are waiting for news about possible changes in oil production policy from OPEC+ countries and the market reaction to macroeconomic factors.

For gold, further dynamics will depend on the dollar exchange rate and bond yields, as well as the general mood in the financial markets at the beginning of the new year.

You have already liked this post today

*এখানে পোস্ট করা মার্কেট বিশ্লেষণ আপনার সচেতনতা বৃদ্ধির জন্য প্রদান করা হয়, ট্রেড করার নির্দেশনা প্রদানের জন্য প্রদান করা হয় না।